Disclosure: This website may contain affiliate links, which means I may earn a commission if you click on the link and make a purchase. I only recommend products or services that I personally use and believe will add value to my readers. Your support is appreciated!

SHARE

Do you like discounted stocks? What do you think of an 84% reduction? This is the amount of shares in a streaming TV technology company Roku(NASDAQ:ROKU) are down from their pandemic-induced 2021 peak. In fact, this stock has barely moved since the second half of 2022, with most investors seemingly afraid to jump in without more evidence that a rebound is underway.

However, as the old saying goes, you should be afraid when others are greedy. The time to be greedy is when others are afraid.

That’s a long way of saying the crowd is looking past a great opportunity here.

The prevailing concern is understandable. After all, the company is not profitable and is unlikely to become so in the immediate future. Investors can also clearly see how crowded and competitive the streaming industry has become.

Still, for interested buyers who can stomach the risk, Roku remains an attractive prospect at its discounted price.

But first.

In case you’re not familiar with it, as has been noted, Roku is a streaming TV technology name. It makes the small boxes attached to your TV that allow you to watch TV shows and movies available through apps like Amazon Prime, NetflixAnd The Walt Disney CompanyIt’s Disney+, to name a few; many televisions are also now available with this technology already built in.

However, televisions and streaming receivers are not its core business. More than 85% of its revenue and all of its gross profits actually come from advertising and servicing its intermediaries for streaming services like the aforementioned Disney+ and Netflix; it also operates its own ad-supported streaming channel. Its devices are only a means to achieve this goal.

Whatever the business model, it works. ComScore data indicates that Roku controls 37% of the U.S. over-the-top (non-cable) connected TV advertising market. Along the same lines, media market research firm Parks Associates reports that Roku accounts for 43% of actively used media playback devices in the country, outpacing Amazon’s comparable FireTV technology. Roku hasn’t yet focused much on overseas markets, but where it has, it has gained respectable popularity there as well.

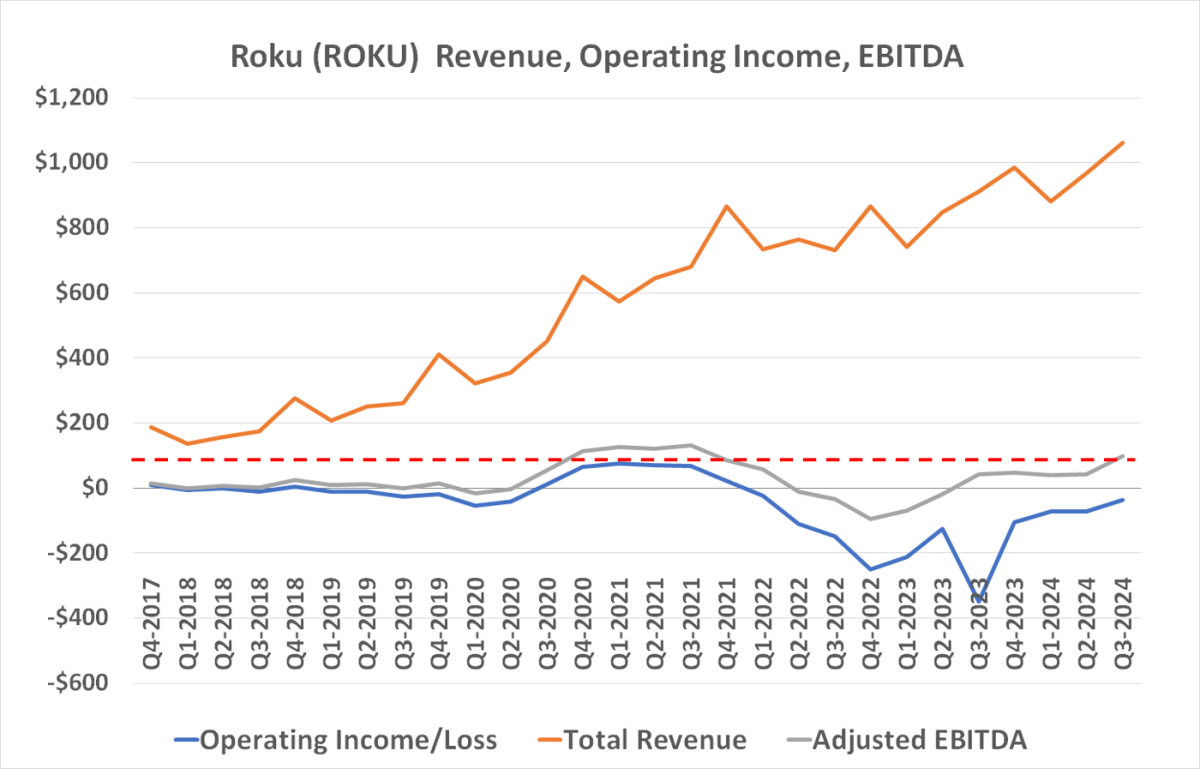

And the company East make progress. Revenues continue to grow and losses continue to decline.

Data source: Roku. The numbers are in millions.

So why doesn’t the title act like this progress has been made? Keep reading.

The extreme uptrend in Roku stock in 2020 is evident. The COVID-19 pandemic was in full swing at the time, stranding millions of consumers at home with nothing to do but watch television. And they did. En masse. For comparison, ComScore reports that live TV viewing in the United States increased by around 70% year over year in March 2020.

Consumers have relied heavily on Roku to facilitate this increase in viewership. Media device sales jumped 35% in the second quarter of 2020 alone, while the number of active Roku accounts improved 41% to 43.0 million for the same period. This breakneck pace of growth will not ease until the second half of 2021.

In retrospect, however, Roku stock’s 540% gain during that period was simply too great. The 2022 bear market has finally forced a much-needed complete correction of this outsized gain. Indeed, the stock has barely moved since then, and many investors are still shocked by the magnitude of the setback.

However, this is one of those relatively rare cases where the lag that allowed for a much-needed correction has persisted for too long. The underlying company has proven that financial viability is possible although it will still take a few years to get there; The analyst community is calling for a move towards positive earnings for the full year 2026, when the company is expected to achieve revenue worth $5.3 billion.

Data source: StockAnalysis.com. Table by author.

Of course, the bulk of this activity will still be ad revenue – the streaming share of overall ad activity that eMarketer estimates accounts for ready to grow at an average annualized rate of 10% through 2027. Roku is well-positioned to enjoy more than its fair share of this growth, taking the company out of the red and black in this relatively short period.

Investors haven’t yet said they’re OK buying stocks to the same extent as they did in 2020, before dumping them in 2022. Analysts aren’t entirely on board either. mass agreement. The majority only view Roku stock as a Hold, while their consensus price target of $83.13 is only about 8% above the stock’s current price. This isn’t really bullish help.

However, neither the analyst community nor investors as a whole are always right about a stock’s likely near and distant future. Sometimes you have to make a judgment that most others don’t seem to completely agree with. This is definitely one of those times.

A guaranteed winner? Certainly not. There is above-average risk associated with the above-average upside potential of this particular ticker. It’s also far from being a fundamental or pillar stock for anyone’s portfolio.

However, there is less risk than the crowd seems to think, and arguably more reward that most see. Sooner or later – and probably sooner that later, the market will have little choice but to reconnect that stock to the continued growth of the underlying company. It would be better to have Roku stock before this starts to happen rather than being forced to chase it higher once the big move finally starts to unfold.

Have you ever felt like you missed the boat by buying the best performing stocks? Then you will want to hear this.

On rare occasions, our team of expert analysts issues a “Doubled” actions recommendation for businesses that they believe are on the verge of collapse. If you’re worried that you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:If you invested $1,000 when we doubled down in 2009,you would have $348,216!*

Apple: If you invested $1,000 when we doubled down in 2008, you would have $47,425!*

Netflix: If you invested $1,000 when we doubled down in 2004, you would have $480,681!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. James Brumley has no position in any of the stocks mentioned. The Motley Fool holds positions and recommends Amazon, Netflix, Roku and Walt Disney. The Motley Fool has a disclosure policy.