Disclosure: This website may contain affiliate links, which means I may earn a commission if you click on the link and make a purchase. I only recommend products or services that I personally use and believe will add value to my readers. Your support is appreciated!

SHARE

(Bloomberg) — It’s a distant project at best, but one that has emerged among a group of diehard bond traders — that the Federal Reserve’s next interest rate decision will be a hike, not a decline.

Most read on Bloomberg

The bet, which was made after the release of a jobs report on Jan. 10, stands in stark contrast to Wall Street’s consensus for at least one rate cut this year. That contrarian bet remained in place even after a subdued inflation report released Wednesday reinforced the Fed’s rate-cutting policy and caused U.S. Treasury market yields to fall from their highest several years high.

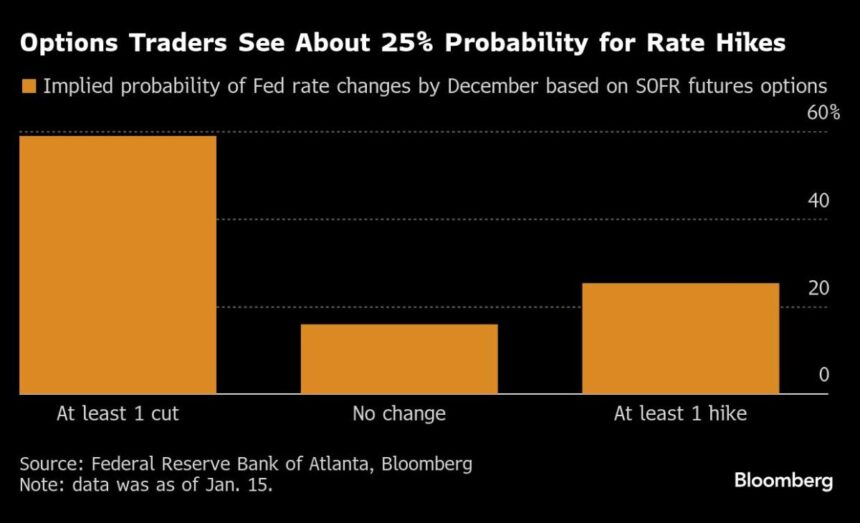

Based on options tied to the Secured Overnight Funding Rate, traders currently estimate there is about a 25% chance that the Fed’s next move will be to raise rates by the end of the year, according to a Bloomberg Intelligence analysis as of Friday’s close. These bets reached 30% before the consumer price data. Until more than a week ago, a hike wasn’t even on the cards: 60% of options traders were betting on further Fed cuts and 40% on a pause.

As with many things in financial markets these days, this is actually a bet on the policies of future President Donald Trump. And it’s based on the idea that tariffs and other policies imposed by the new administration will trigger a rebound in inflation that will force the Fed into an embarrassing about-face.

Phil Suttle, a former New York Federal Reserve economist who now runs his eponymous consulting firm, believes the Fed will raise rates in September. “I have them not cutting at all. And it’s not a mad dog view,” he said Friday on the Macro Hive podcast.

Suttle expects Trump, who takes office Monday, to pass tariffs and restrict immigration, thereby increasing inflation. The United States is already starting to see wages rise again, he said.

For now, Suttle’s view remains extreme. Bond traders fully priced in a quarter-point rate cut for this year and saw about a 50% chance for a second cut, compared with just one cut a week earlier. On Thursday, Fed Governor Christopher Waller said policymakers could cut rates again in the first half of 2025 if inflation data remains favorable.

Those remarks sent U.S. government bond yields lower. Earlier last week, the benchmark 10-year Treasury peaked at 4.81%, its highest level since late 2023. Long-term yields have risen since the Fed began cutting rates in september.

“If you were to see significant inflation surprises over the next few months, you might have a market that starts flirting with the possibility of a rate hike this year,” said Roger Hallam, global head rates at Vanguard.

After the December policy meeting, Chairman Jerome Powell told reporters that the central bank was not willing to settle for inflation above its 2% target. Asked if that meant they couldn’t rule out a rate increase in 2025, he said: “You don’t completely rule out things in this – in this world.” » He added, however, that an increase “does not seem to be a likely outcome.”

Even though the bar for rate hikes is high, the Fed has already quickly reversed course. In 1998, authorities cut rates three times in quick succession to short-circuit a financial crisis caused by Russia’s default and the near collapse of the hedge fund Long Term Capital Management. The Fed then began raising rates in June 1999 to contain inflationary pressures.

“What the market would need to meaningfully price in hikes is for inflation to really pick up – with, for example, consumer prices reaching an average level of 3%,” said Tim Magnusson, director investments from hedge fund Garda Capital Partners. “I think the Fed is very comfortable sitting on its hands for a while.”

Benson Durham, head of global asset allocation at Piper Sandler and a former Fed economist, estimates that a probability of just under 10% is built into money market options for at least one rate hike this year, when contracts are adjusted based on the term premium, the excess return that investors are supposed to demand to buy longer-term securities, an analysis the Fed has also used for a long time, he said .

“Overall, it appears that the market is quite balanced against the current risks of increases or reductions,” he said.

What to watch

Economic data:

January 21: Philadelphia Fed non-manufacturing activity

January 22: MBA mortgage loan applications; Leading Index

January 23: first unemployment registrations; Kansas City Fed Manufacturing Activity

January 24: S&P global manufacturing PMI in the United States (preliminary); S&P Global US Services PMI (preliminary); S&P Global US Composite PMI (preliminary); University of Michigan Sentiment (final); sales of existing homes; Kansas City Fed Services Activity

Fed Timetable:

Auction schedule:

January 21: invoices for 13, 26 and 52 weeks; 42 day CMB

January 22: 17-week bills; 33-day CMB; Reopening of 20-year bonds

January 23: invoices 4 to 8 weeks; ADVICE over 10 years