Disclosure: This website may contain affiliate links, which means I may earn a commission if you click on the link and make a purchase. I only recommend products or services that I personally use and believe will add value to my readers. Your support is appreciated!

SHARE

With Donald Trump entered the presidency, an opportunity is on the horizon for the energy sector. Many are waiting More favorable policies To lead to exploration and drilling in the United States, which could open the way for expansion opportunities for oil and gas companies.

An area to be monitored is energy stocks in the middle of the race. These companies play an essential role in the energy supply chain, specializing in the collection, processing, transport, storage and export of oil and gas. Intermediate operators want to gain an increase in production, and investors in energy equity in the environment should today consider it is Energy transfer(Nyse: and). Here is why.

Energy transfer is a power station in the in the middle sector, specializing in transport, storage and terminal operations of vital energy products, including natural gas, crude oil, natural gas liquids (LGN) and liquefied natural gas (GNL). The company has a large network of pipelines and storage facilities, guaranteeing an effective movement of natural gas from production sites directly to public services, industrial customers and other pipelines.

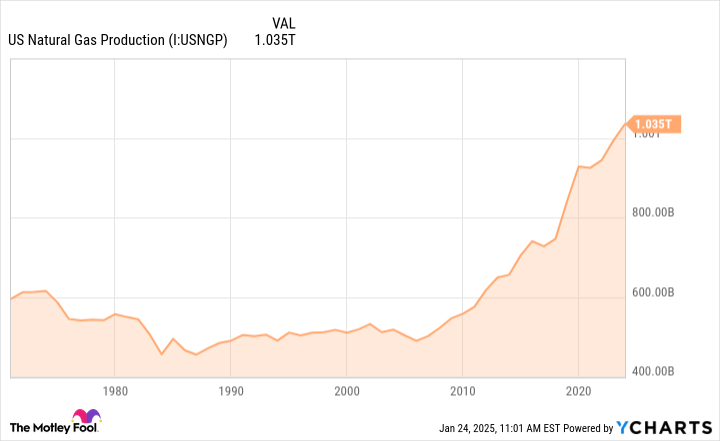

What distinguishes energy transfer is that it is one of the largest median integrated operators in the United States, and recent trends have benefited him a lot. Since the years 2010, the United States has experienced an explosion in natural gas production, powered by the progress of hydraulic fracturing (also called hydraulic fracturing) and horizontal drilling techniques – which have exploited large reserves of gas from shale.

The United States has made significant progress in the production of natural gas, reaching 1,035 billion cubic meters in 2023, thanks to the improvement of extraction techniques. Not only that, but many see natural gas as a bridge fuel to pass higher carbon sources such as coal to more renewable sources such as wind, solar and nuclear energy. Natural gas emits around 50% carbon dioxide less than coal.

With stable sources of stable income generated by transport costs and storage services, energy transfer is well positioned to benefit from the growing volumes of products that circulate through its systems. The company has also made movements to increase its natural gas infrastructure footprint.

The company has made a positive final investment decision for the construction of the Hugh Brinson pipeline through the center of Texas. Previously known as Warrior Pipeline, this infrastructure will connect the Permian basin to the main markets and shopping centers, improving transport capacity to meet the growing demand for natural gas.

This project will be completed in two phases. In the first phase, 200 miles of pipeline will be built, with a capacity of 1.5 billion cubic feet per day (BCF / D). This part of the project should be in service by the end of 2026. In phase two, the capacity of the new pipeline would be increased to around 2.2 BCF / J. Construction will cost around $ 2.7 billion.

Image source: Getty Images.

In other news, energy transfer makes solid progress with its export plant at Lake Charles in Louisiana. The company, which has spent years securing customers to market this installation, has concluded a 20 -year -old LNG sales and purchase agreement with Chevron. As part of the agreement, the energy transfer will provide Chevron 2 million tonnes per year (MTPA) of capacity.

The demand for natural gas increases and the transfer of energy is well placed to capitalize on this growth. The US Energy Information Administration provides that natural gas demand in the United States will increase more than supply. In its forecasts, the demand for agency projects will increase by 1.4 BCF / D while demand increases by 3.2 BCF / J, mainly due to increasing exports.

Investors must remember that energy transfer works as a Master Limited Partnership (MLP). This structure offers investors, including coherent cash flows and attractive distribution returns. However, it is also delivered with specific reporting requirements that could delay and complicate your taxes on the tax season.

That said, energy transfer is one of the largest operators in a median environment in the United States and is a fairly reasonable price compared to its peers. The MLP has also done a good job by expanding its footprint, and a more favorable regulatory environment should increase well for its future – which makes it a solid energy stock for investors to consider buying today.

Before buying energy transfer actions, consider this:

THE Motley Fool Stock Advisor The team of analysts has just identified what they believe 10 Best Actions For investors to buy now … and energy transfer was not part of it. The 10 actions that cut could produce monster yields in the coming years.

Inquire Nvidia Make this list on April 15, 2005 … if you have invested $ 1,000 at the time of our recommendation, You would have $ 874,051! *

Now it’s worth notingStock advisorTotal average yield is937% – an outperformance that has made the market compared to178%For the S&P 500. Do not miss the last list of the best 10.