Disclosure: This website may contain affiliate links, which means I may earn a commission if you click on the link and make a purchase. I only recommend products or services that I personally use and believe will add value to my readers. Your support is appreciated!

SHARE

The last five years have been fruitful during Advanced micro-apparents(Nasdaq: AMD) Investors, as an investment of $ 1,000 made in stocks a half-decade ago, is now worth nearly $ 2,200 when writing this article.

However, to put things in perspective, the leap of 118% of AMD shares in the past five years is lower than the 178% jump is timed by the Phlx semiconductor sector Index over the same period. The past year was particularly difficult for AMD investors, because the action lost 41% of its value during this period. This large drop can be attributed to the inability of AMD to capitalize on booming demand for Artificial Intelligence (AI) Chips, a market where the Rival Arch Nvidia has established a dominant position.

But then, the recent results of AMD were solid, and the company has more than one catalyst that could help revive its stock market in the next five years. We will take a closer look at the potential AMD growth engines and check why it can be a good idea to buy and keep this stock for the next five years.

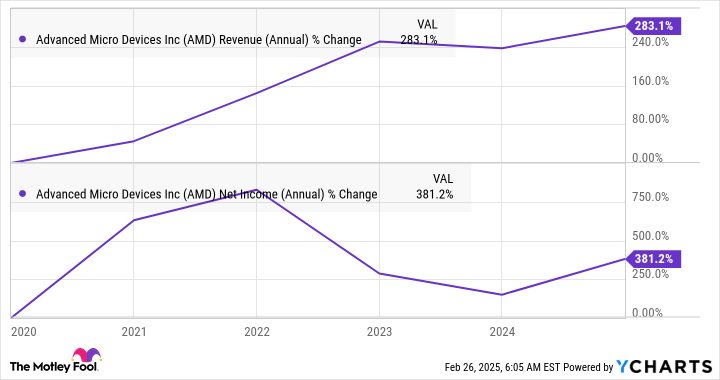

AMD’s financial performance in the past five years has been mixed. While the income and profits of the company increased in 2020, 2021 and 2022 due to high sales of its central processing units (CPU) and graphics cards used in personal computers (PC), its growth in results failed after a good start.

This is because the PC demand decreased After solid sales in the years of the new coronavirus pandemic. AMD ended up with an excess inventory on his hands, and he had to write it, resulting in a sharp drop in business income. Meanwhile, the activity of the company data center was in good shape throughout this period, because it continued to win from the CPU server Intel.

But then, sales of game consoles from Sony And MicrosoftWho are fed by the semi-personalized processors of AMD, began to mature and led these technology giants to place fewer commands. Add the fact that AMD is well behind Nvidia on the game graphics card market, with a share of only 10%; It is easy to see why business game activities are struggling for traction.

Thus, the mixed performance of the various AMD companies has weighed on the performance of the title in the past five years. However, the good news is that all the segments discussed above are likely to benefit from solid growth over the next five years, paving the way for a greater increase in AMD actions.

AMD’s performance over the next five years will depend on the health of key segments such as games, data centers and PCs. The right part is that all of these corporate segments are likely to take advantage of secular growth thanks to various catalysts.

The business game activity, for example, should benefit from the arrival of new Microsoft and Sony game consoles. The current console generation is almost five years old. A new one is expected to arrive in the next two to three years because Sony and Microsoft have historically published a new generation of consoles every seven to eight years.

Sony and Microsoft should publish their new generation consoles in 2026 or 2027.

Passing from games to PCs, AMD has already started to see a solid traction on this market. Revenues from the company’s customers segment increased 52% in 2024 to a record of $ 7.1 billion, thanks to the “high demand for AMD Ryzen processors in the office and the mobile”. The prospects for the PC market for the next five years seem to be brilliant due to the advent of the generative AI.

According to an estimate, IA PC market income should jump nearly 5x between 2024 and 2030. This is a good business for AMD’s long -term prospects, in particular because the company has obtained a larger market share of the PC processor. The flea manufacturer finished 2024 with almost 25% of the customer processor market under its control, up nearly five percentage points compared to the period of the previous year, according to Mercury Research.

Its share of income from the customer PC market has increased at a faster rate, which increases 8.4 percentage points from one year to another. This points to the improvement of the AMD pricing power on the PC processor market, because its share of income improves at a faster pace than the share of the unit. In addition, it will not be surprising to see AMD win more market share, because Intel-Rival should not launch a new office CPU before next year.

As such, the scene seems ready for healthy growth in AMD games and PC segments over the next five years. At the same time, the activity of the company’s data center is also improving, even if it plays the second NVIDIA violin on the GPU AI market (Graphics Processing Unit). The income from the AMD data center almost doubled last year for a record of $ 12.6 billion, pulled by solid sales of its server and GPU processors.

The company has sold at least $ 5 billion in data center GPU in 2024. AMD plans that its GPU activities in the data center could reach “tens of billions, over the next two years.” In fact, AMD could invite solid revenues to the GPUs of the long-term data center, even if he manages to wedge a small part of this market for himself.

In the end, we can conclude that AMD seems ready for growth in current profits over the next five years. This is why the purchase of this stock seems to be obvious at the moment, in particular given its price / benefit / growth / growth ratio (PEG ratio) of only 0.42 depending on its growth in the expected profits over five years, according to Yahoo! Finance.

A PEG ratio of less than 1 means that a stock is undervalued in light of the growth it should offer, and AMD is negotiated well below this threshold. Thus, investors who seek to buy a growth actions that are negotiated at attractive levels can consider adding DMA to their wallets. This stock seems to be positioned for an impressive long term increase.

Have you ever had the impression of having missed the boat to buy the most successful actions? So you will want to hear this.

On rare occasions, our team of analysts experts issues a The “Double Down” stock Recommendation for the companies they think are about to burst. If you are afraid, you have already missed your chance to invest, it’s the best time to buy before it is too late. And the figures speak for themselves:

NVIDIA:If you have invested $ 1,000 when we doubled in 2009,You would have $ 323,920! *

Apple: If you have invested $ 1,000 when we doubled in 2008, You would have $ 45,851! *

Netflix: If you have invested $ 1,000 when we doubled in 2004, You would have $ 528,808! *

Currently, we are issuing “double” alerts for three incredible companies, and there may be no luck like this as soon as it is.

Hack Has no position in the actions mentioned. The Motley Fool has positions and recommends micro advanced devices, Intel, Microsoft and Nvidia. The Motley Fool recommends the following options: Long January 2026 $ 395 Calls on Microsoft, short February 2025 27 $ calls Intel and short January 2026 405 $ calls Microsoft. The Word’s madman has a Disclosure policy.