When interest rates are high, people are supposed to think twice before the loan. When they are low, they are supposed to take out the metaphorical (or literal) credit card. It is the central idea Sub-full the monetary policy of central banks.

Of course, central banks only set the short -term interest rate. LeapAlthough anchored by central banks’ rates, are established on the secondary market thanks to a sort of continuous auction process. And in a world where government obligations make describe the probable course of the future action of the Central Bank, a government should be indifferent to its presence on this curve.

According to some long recent reports of rate strategists, Moyeen Islam of Barclays and Mark Capleton by Bank of America – is not the world in which we live.

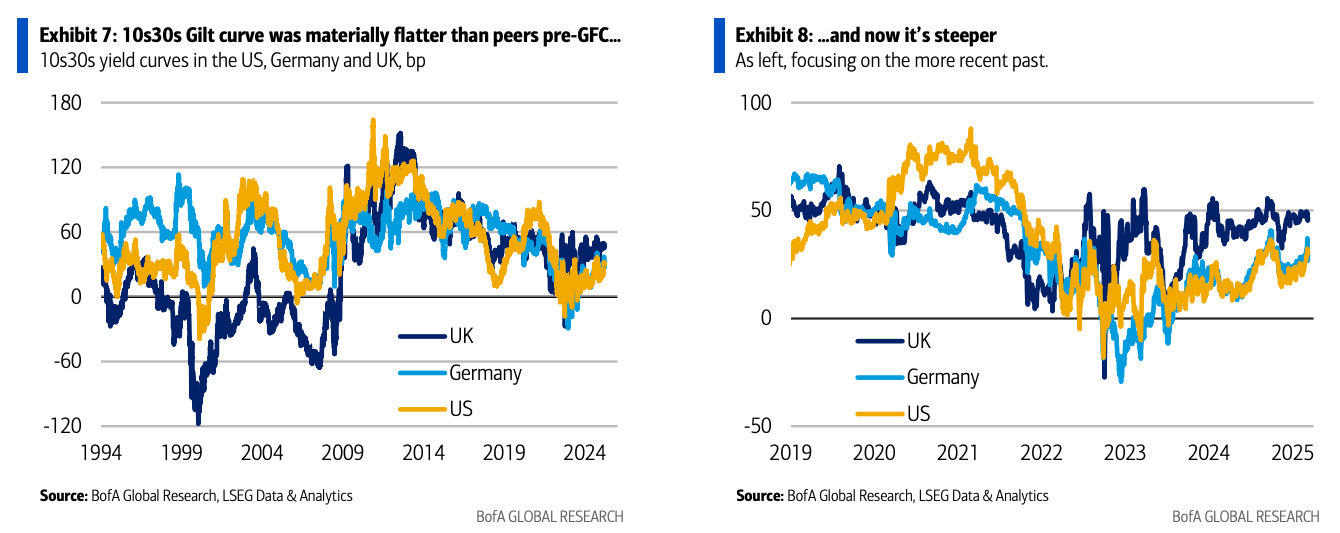

Before the global financial crisis, ten years’ nicknames have often given more than thirty years (contrary to conventional logic this longer duration = more risk = more yield). Most types of bonds have understood this as the reflection of the persistent demand for British life-life insurers and pension funds that pursue passive investment strategies. As such, it was logical that HM Treasury changed their debt emission longer, responding to this request and reducing their own so-called “risk of refinancing”. In doing so, the United Kingdom has ended up with the highest average government bond market in the world.

Rapid advance in the post-federal era, and the longer term licks are negotiated with a yield not only higher than the 10-year lifts, but also with a yield propagation greater than 10s, which is higher than those of the United States or Germany. Graphics via Bofa:

Despite Capleton’s “skepticism on the question of whether intelligent mathematical chromatography can really make a yield in conjunction and deconstruct it in different unobservable (and perhaps hypothetical) components”, he believes that this new yield space represents a great term of big terms – aka a sure sign that long efforts are dear to emit. He saves his point of view with a pile of Gilts-Sonia forward and propagation graphics forward which are too geek even for FT Alphaville.

Barclays Islam has no such scruples about directly by declaring that Rising Term Premia “explains most of the movement above [thirty-year] given “.

Why could it be? Many are based on the 800 lb gorilla of a question suspended on the market for long -term nods: if the long -standing request for British pension funds is almost complete. While ‘Peak ldi‘ has been called Before, the arguments are worth spelling.

First of all, the passage of the so-called massive “desire” of the passage of actions to the obligations which has been the scourge of the existence of every last two decades of the director of British actions for two decades. This cannot happen again. The amount of potential to come is, according to Capleton, minimis.

Second, with pension schemes defined almost all closed to the new entrants, people retire and finally die. This now appears in the narrowing of membership data. As Capleton writes:

The version “financed by the US in the United Kingdom” shows that total membership dropped by 16% between 3T 2019 and 1T 2024, and in total, the composition is aging, the proportion of retirees going from 42% to 49% over this same short period.

Third, the current value of retirement funds has been Absolutely aisé By … the increase in bond yields. So, if each defined advantages regime invests all of its assets in nods, that would only represent approximately one billion of demand books, against a request ceiling of approximately two billions of books a few years ago.

The main thing is that there is no new request for retirement funds for long -term nearby checks. And this fact appears in bond prices.

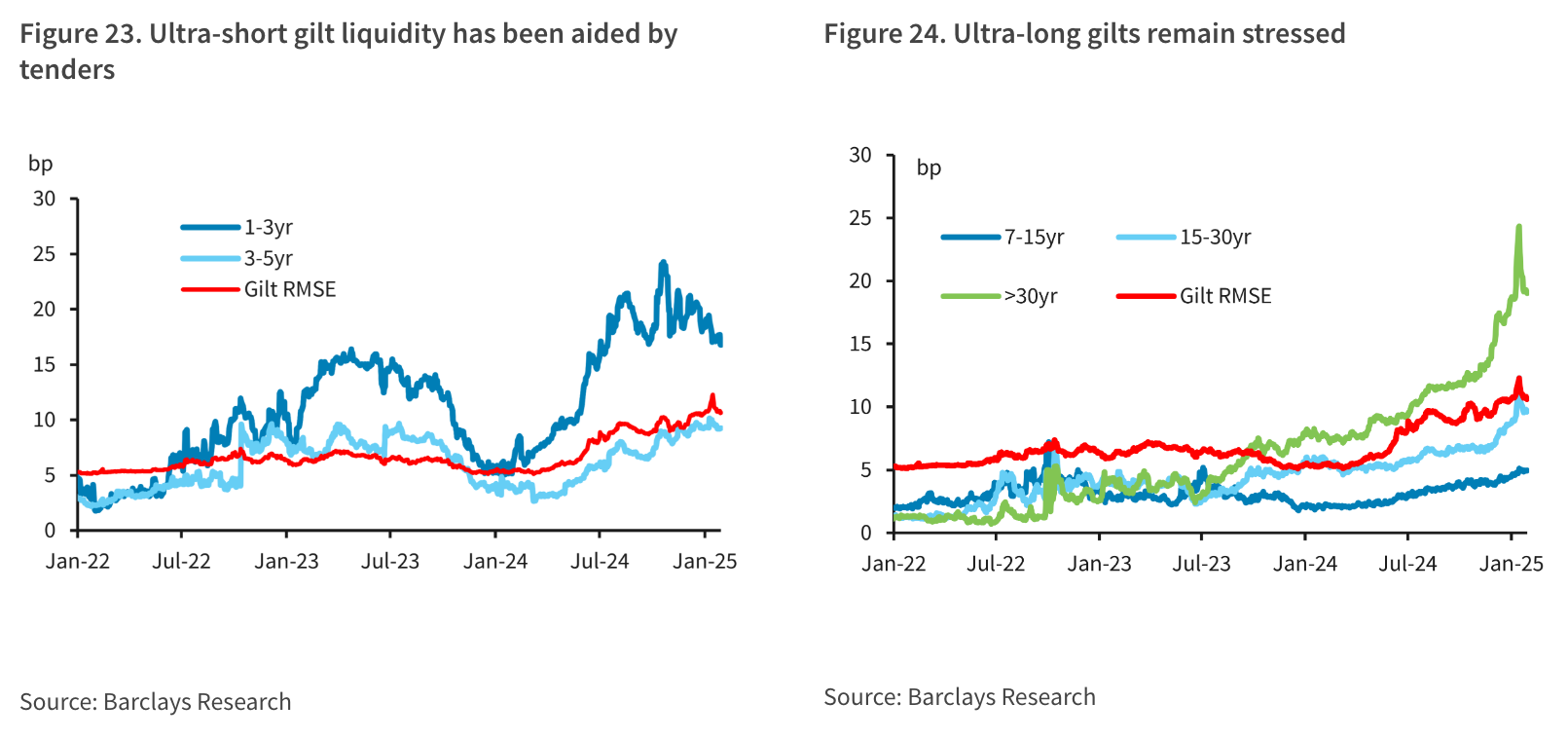

Barclays argues this point with mathematics. Although golden auctions went pretty well, the market capacity to digest the risk is, supports Islam, function of the underlying liquidity. A way in which Barclays takes a measure is by drawing lines along different parts of the golden yield curve and calculating the Racine Square Errors which are generated from these lines of the best fit. The underlying intuition is that in a massively liquid market, all folds will be arbitrated.

But that doesn’t happen. And the part of the curve where this liquidity measure has deteriorated rapidly along the range. Last year We have pointed out The increase in the relevance of the curve as having perhaps something to do with an offer for the tax advantages attached to the low coupon licks. But it seems that something else happens too. Barclays:

As such, the Capleton de Bofa estimates:

The golden show must adapt, radically and quickly. … This pleads for a material reduction in the golden issue on a long time.

And this essentially places them on the same wavelength as Barclays.

It is not as if the governments had not made major changes to the emission previously on the back of long -standing bonds more and more expensive. Older readers will remember that Halloween in 2001, the US Treasury caused a massive liaison rally when it Canceled any long connection broadcast until further notice. Defending the decision, Peter Fisher, then the secretary of the Treasury, explained that:

It’s about trying to carefully manage taxpayers money. … It is a relatively expensive borrowing tool that is simply not necessary for current funding requirements or those we expect.

In addition – as Capleton reminds those of us under the age of state retirement – the American decision was an echo of Geoffrey Howe’s decision to cancel the long -term emission in its 1983 budget. And while Barclays strikes a measured tone – encouraging the DMO to shorten the duration of its issue to improve market liquidity and reduce taxpayers – these more radical examples The long -term emission are those that Bofa estimates that the DMO should examine closely today.

Rather than issuing costly long -term bonds whose main beneficiaries are literally dying, the Bofa recommends moving the program to British Treasury bills. The UK UK market is quite breathtaking according to the international standard, and Capleton argues that the quantitative tightening is evolving, there will be a large demand for invoices of banks that seek to find substitution assets that behave like Bank of England reserves.

Barclays and Bofa [ed: try saying that several times quickly] Make sure that the British government, if it was a business, would review and shorten its debt emission profile.

Capleton also raises the idea that they should buy long-standing licks that are negotiated with a significant discount, “taking profits” on the bonds sold on the market with weak coupons, and perhaps retracting up to 16% of debt / GDP in the process.

But he jumps the shark when he writes:

With some of these problems, the obvious temptation would be to consult the market. Our main concern with this is the risk that action is delayed, potentially for a long time, if it is a very formal consultation process … We suggest experimental operations rather than full -fledged consultations.

Experience rather than consulting? Sorry, we are British.

Overall, these are two fascinating and imaginative reports full of interesting debt management ideas. But if the British government reacts to the signals of bond market pricing in the way in which normal economic agents are supposed to make is another question.

Non-liability clause: The author has assets with direct among his personal investments, one of which has long been. 😢

{kind=link}

{kind=link}

{kind=link}